In my previous post, we discussed the logistics and costs of in-person sales events, so today we are revisiting managing our expenses. I did cover this a few months ago, so if you already have seen this, thank you for stopping by!

If you intend to make personal appearances at local bookstores, fairs, or conventions, you should have an inventory of books to manage and account for at the end of the year. You will have expenses to report. This can be quite a headache if you have more than one or two books to track.

The good businessperson has a spreadsheet of some sort to account for this side of the business, as it will be part of your annual business tax report. An excellent method for assembling the information we generate for your tax report is discussed in a guest post by Ellen King Rice, The Business Sequence for Writers. Her article offers an excellent framework for keeping our business records straight, so filling out our annual tax forms will be easy.

The good businessperson has a spreadsheet of some sort to account for this side of the business, as it will be part of your annual business tax report. An excellent method for assembling the information we generate for your tax report is discussed in a guest post by Ellen King Rice, The Business Sequence for Writers. Her article offers an excellent framework for keeping our business records straight, so filling out our annual tax forms will be easy.

As a former bookkeeper, I strongly suggest you keep an account of your costs for each book. This is for tax and insurance purposes if the stock of books is lost or damaged in a house fire or flood.

You can do this on notebook paper with a pencil, a ruler, and a calculator. However, a green or yellow ledger book with eight to twelve columns is already set up for you to begin using. These are available at Amazon and can be found at all office supply stores and some grocery stores.

I began working as a bookkeeper in 1982, using the industry-standard tools of the trade for the time. We noted each transaction with a red or black pencil in ledger books of varying sizes (2 to 32 columns). In those days, we used rulers or yardsticks to ensure we tracked a particular item on the correct line across all the columns. The handiest electronic device on my desk was the calculator with a printout tape.

The tools for this method of accounting are still available in the stationery section of any store and are quite affordable.

I use Excel for all my accounting purposes, but no matter how you create your spreadsheet, each title you have on hand to take to book fairs or shows has several associated costs.

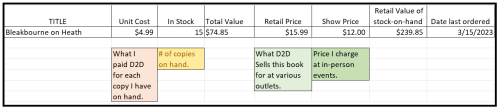

The first column contains the heading Titles: under that heading, list the title of each book you take to shows. We will use my most recent book, Bleakbourne on Heath, as our example book.

On the same line as the word Titles, working to the right in column 2, write unit cost. This is the price you pay for each copy you must take to a show and varies from title to title by the book’s length and trim size. On the same line as the book’s title, write the cost you pay D2D, KDP, Ingram Sparks, or your publisher for that paper book. In this case, I pay Draft2Digital $4.99.

Column 3 is the current stock-on-hand at the end of the taxing quarter: Quantity in stock: 15

Column 4 is the sum of column three times column two: Inventory value: $89.11. That is what you would have to pay to replace those books. It is also what some Departments of Revenue may tax you on at the end of the year if the value of that stock is over a specific limit, say $5,000.00. The total value of stock-on-hand for all my books combined rarely exceeds $500.00.

Column 4 is the sum of column three times column two: Inventory value: $89.11. That is what you would have to pay to replace those books. It is also what some Departments of Revenue may tax you on at the end of the year if the value of that stock is over a specific limit, say $5,000.00. The total value of stock-on-hand for all my books combined rarely exceeds $500.00.

Annual inventory taxes are why retail stores have end-of-the-year sales. They need to offload their inventory to keep their taxes low.

Column 5 is the retail price. This is what Draft2Digital charges for the book: $15.99. You set your retail price to cover the cost of replacing the book, with some revenue to cover table and vendor fees at shows and conventions (see my previous post, the Business Side of the Business: budgeting for in-person sales events,) and still allow for a small profit.

Column 6 is the special show price (if you discount your books at shows): $12.00.

Column 7 is the retail value of your stock on hand. It is the sum of column 3 times column 6: $228.00.

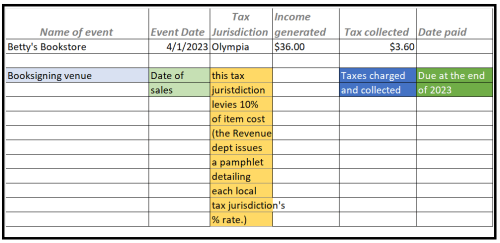

Did you collect sales tax from your customers? When you apply for your business license, you will receive a pamphlet with all the taxing jurisdictions in your licensing area and their tax rates. These range between .08 and .11 here in Thurston County.

Washington State has no income tax, so all our revenues come from quarterly business and sales taxes collected at the time of purchase.

Note the tax jurisdiction where the books were sold, as you may be required to forward the taxes collected to your state or province’s Department of Revenue. If you are smart, you will make another page with these columns:

At the bottom of both spreadsheets, total each column. That will give you the stock expenses for all your titles. There will be no scrambling at the end of the quarter for Business and Occupation taxes if you live in a state like Washington State or at the end of the year if you live elsewhere. Be smart and set aside the money collected as sales tax because it is not yours and is not part of your income.

That way, you will have it at the end of the year if you only do a few shows a year like me, or quarterly if you do shows and signings every week.

Bookkeeping should take less than an hour after each show. If you have kept your spreadsheets updated, filling out annual business tax forms for your state and federal agencies will go quickly. You will have all the numbers you need to back up your reports if you are audited.

Also (and this is important), you will know the exact number of books you have on hand in each title. You will know when it’s time to reorder more stock. There is a two-to-three-week lag in printing and shipping time, so ordering books in advance is critical. You don’t want to waste money by purchasing stock you have plenty of, but you need to have a supply of your better sellers.

My personal spreadsheet is a little more detailed and is saved in the cloud, as are all my business and other records. I also back up my files to an external drive because it never hurts to be vigilant.

Something we rarely consider is the infrequent natural disaster. I live on the northwest coast of the US, so we must sometimes deal with forest fires, earthquakes, volcanic eruptions, Pacific hurricanes, and, occasionally, tornadoes. They don’t happen often, but it can be devastating when they do.

Depending on where you live, the natural world can be hazardous. If something should happen to your stock of books due to theft, fire, or flood, you will be able to claim your business loss.

Depending on where you live, the natural world can be hazardous. If something should happen to your stock of books due to theft, fire, or flood, you will be able to claim your business loss.

Many authors are far more prolific than I am. Replacing the stock of 1 to 30 titles is a burdensome expense to carve out of the family budget unless an author has sold enough to cover that cost.

Are you covering your costs? Keeping good records will ensure you can see where you stand and allow you to make good decisions regarding your expenses.

At first, getting your books in front of readers is a challenge. The in-person sales event is one way to get eyes on your books. This could be at a venue as small as a local bookstore allowing you to set up a table on their premises.

At first, getting your books in front of readers is a challenge. The in-person sales event is one way to get eyes on your books. This could be at a venue as small as a local bookstore allowing you to set up a table on their premises.

The final thing you will need is a way of accepting money. I have a metal cash box, but you only need something to hold cash and some bills to make change with. A way to accept credit cards, something like

The final thing you will need is a way of accepting money. I have a metal cash box, but you only need something to hold cash and some bills to make change with. A way to accept credit cards, something like  I suggest buying book stands of some sort. Recipe stands work, as do plate and picture stands. Whether they’re fancy or cheap, be sure you know how to use them properly so they aren’t falling over when someone bumps the table. I use folding plate stands as they store well in the rolling suitcase I use for my supplies.

I suggest buying book stands of some sort. Recipe stands work, as do plate and picture stands. Whether they’re fancy or cheap, be sure you know how to use them properly so they aren’t falling over when someone bumps the table. I use folding plate stands as they store well in the rolling suitcase I use for my supplies. If you plan to get a table at a large conference this year, I highly recommend

If you plan to get a table at a large conference this year, I highly recommend